What’s the Average Student Loan Debt in Canada? 19 Staggering Statistics

By

February 5, 2024

12 min

quick answer

The average student loan debt in Canada is $28,000. With factors like gender, age, location, and program of study impacting the amount of debt a borrower takes on, many people can’t afford to pursue post-secondary education but also can’t afford not to.

In This Article

With the average student loan debt in Canada at approximately $28,000, it’s no wonder 77% of Canadians under 40 say they regret taking out student loans.

Student loan forgiveness is not an option for most borrowers, so they’re forced to spend an average of 9 1/2 years paying off their loans — which is, in most instances, more than double the amount of time they would’ve spent in school.

But, with increased demand for college education, students are willing to take on debt for the potential benefits, such as better earning potential and more job opportunities.

However, is the cost of debt worth the ultimate price? Read on to learn about student debt in Canada and how it’s impacting the entire country.

|

Key Takeaways:

|

Student loan debt has steadily increased across Canada since 2000, from the total amount borrowed to individual debt. The amount of individual debt depends on a variety of factors, such as the specific program, level of education, and school location.

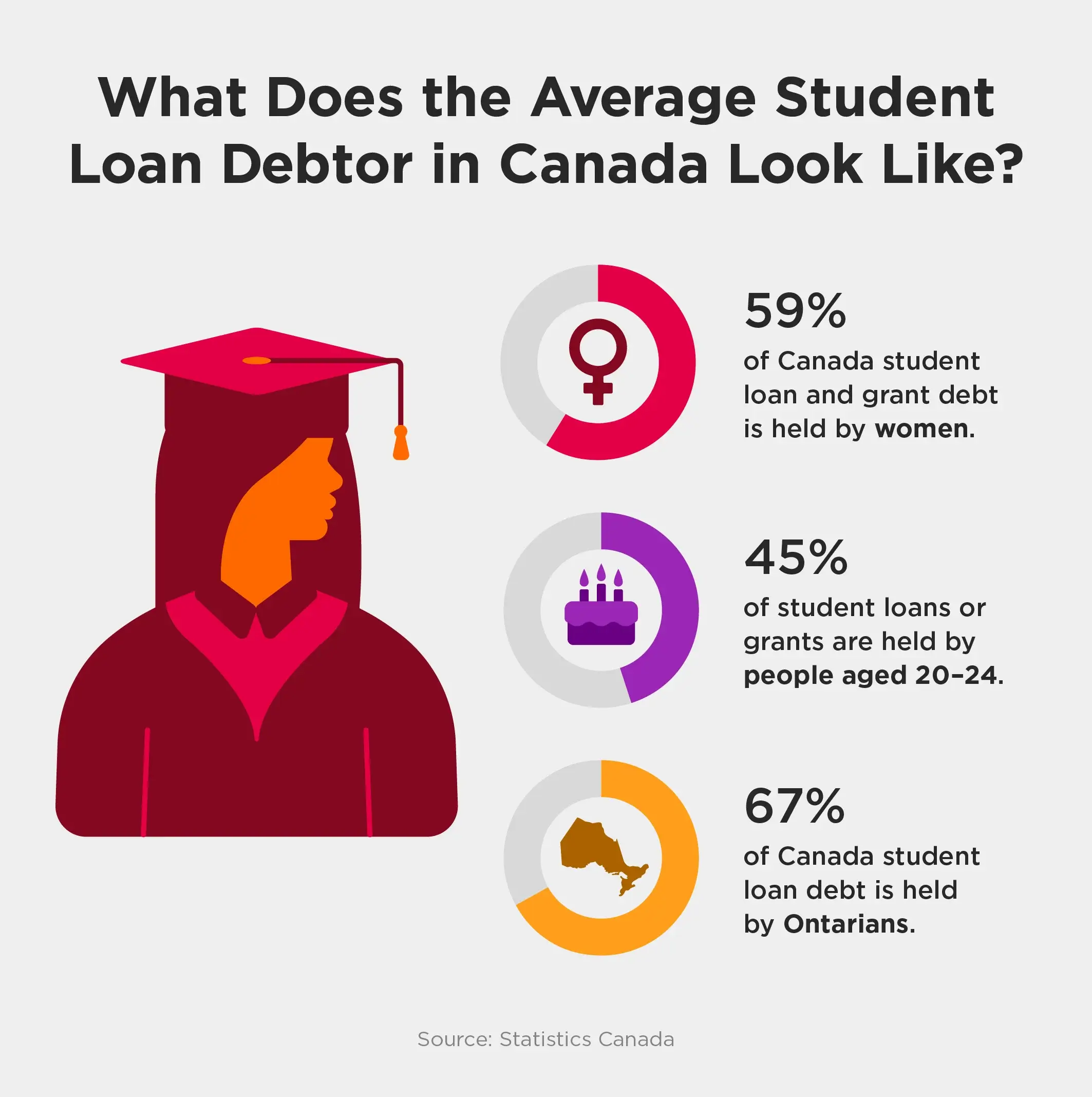

So how many Canadians currently have student loan debt? Approximately 625,000 Canadians receive a Canada student loan every year. Undergraduate students are the most likely to take on student loans, as are female students. Here’s a breakdown of Canadians with student loans:

The total student debt in Canada amounts to billions of dollars. With the increasing demand for college education in the job market, this number only goes up year over year. Here are some facts about total student debt in Canada:

The average cost of university tuition in Canada for both undergraduate and graduate programs was $7,135.50 per year for the 2022/23 academic year. The cost of university tuition varies greatly depending on the specific program, as well as the location.

Unsurprisingly, the highest tuition rates are for professional degree programs, such as law and medicine. While this is in part because of their specialized nature, it’s also due to their potential returns (both perceived and actual), as average annual salaries for these roles can range from $77K to $134K. Professional programs may offer students better career opportunities and potential earnings.

Post-graduate programs in Canada can also be quite costly. However, with the potential to earn one-third more than those with only an undergraduate, it can be worth the investment for some.

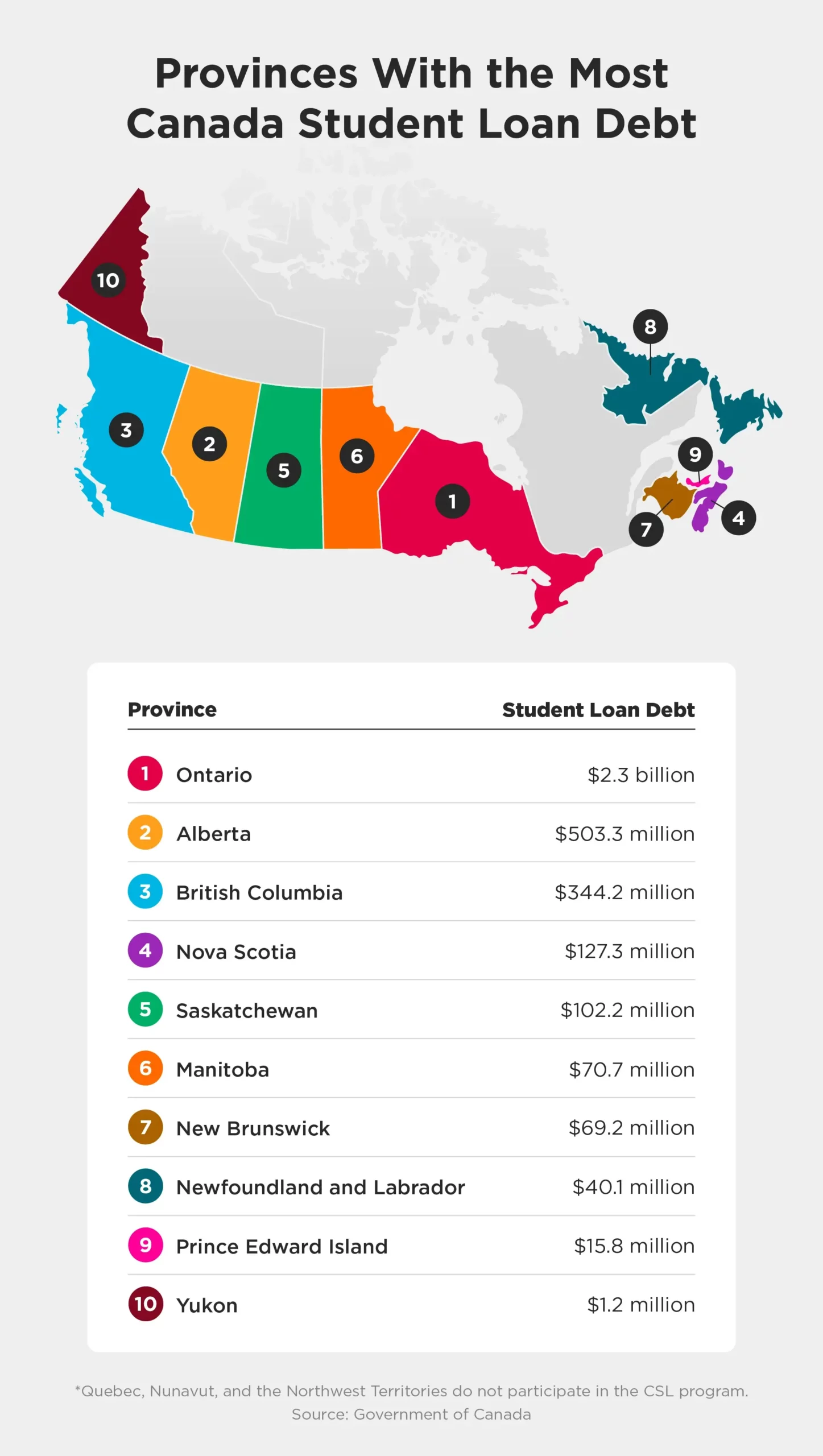

According to the Government of Canada, students in Ontario, Alberta, and British Columbia received the highest amount of student loans from the Canada Student Loan (CSL) program in the 2018/19 academic year.

*Quebec, Nunavut, and the Northwest Territories do not participate in the CSL program.

Many factors contribute to the amount of student loan debt borrowers take on. From the types of loans and grants to inflation rates to the larger economic climate, here are some key factors determining how much student loan debt Canadians accrue.

Students in Canada can apply for grants and loans both at the federal and provincial levels. Federal grants do not need to be repaid. However, the CBC has reported instances where a student’s status changes midway through their program or a student received an excess grant payout, and the student is then responsible for paying it back as though it were a loan.

With the average cost of tuition in Canada increasing — which is rising disproportionally with inflation — it’s no wonder graduates are finding themselves in more debt than previous generations. In fact, tuition in Canada has risen 3.7% over 10 years, while inflation has only risen 1.65% in the same period. These rising costs create a barrier to education access.

While the Government of Canada no longer requires interest payments on federal student loans as of April 2023, provinces are still able to set their own interest rates. Loans acquired before April 2023 will not continue to accrue interest, but the accumulated interest does have to be paid off.

For Canada student loans, students have a six-month grace period at their end of study before they must begin making payments. British Columbia, Manitoba, New Brunswick, Nova Scotia, Prince Edward Island, and Newfoundland and Labrador provincial loans do not have interest fees.

In some provinces where interest still accrues on student loans, there is no grace period, and interest will apply on the student’s study end date. Here’s an overview of how interest and repayment works by province:

As previously shown, certain demographics are more likely to take on student loan debt. Women, those aged 20-24, people from Ontario, and those in undergraduate programs hold a higher proportion of student loans in Canada. Of course, those below a certain economic threshold are also more likely to need student loans to access education.

With high interest and strict payment terms, people are often forced to take on more debt just to stay afloat. Not only that, but ongoing student debt impacts the ability to take out other loans, which can impact your ability to achieve common financial goals like:

Of course, this impacts you as an individual greatly, but it also impacts your ability to fully contribute to the Canadian economy. Here are some of the ways that student loan debt impacts Canadians.

Many new graduates struggle to find a job in their field regardless of their debt status. For new grads with student loan debt, the incurring interest and pending repayment date may force them to take entry-level jobs or lower-paying roles outside of their field.

Research finds that, since 2016, the number of unemployed graduates with partial or complete post-secondary education has exceeded the number of vacant job positions. The Canadian job market simply cannot accommodate the number of graduates.

Canada is facing a debt crisis at the national, provincial, and individual levels. Student loans play a big part in that. Canadians are currently faced with higher costs of living than any previous generation, with wages not rising at the rate of inflation. The reality is that debt begets more debt.

Many are forced to take on more debt to just stay afloat, whether that’s credit card debt, payday-type loans, lines of credit, or other sources of debt. Consumer debt is a slippery slope, as it’s very high interest, and the interest only accumulates.

Insolvency, the inability to make debt payments on time, is on the rise among Canadians, both at the business and consumer levels. 2023 saw a 19.5% increase in consumer insolvency and a 22.8% insolvency increase in businesses from 2022. Student debt plays a big role in insolvency, with nearly 1 in 5 insolvencies in Ontario in 2018 including student debt.

Student debt has lasting impacts on both the individual and society as a whole. From increased instances of mental health issues to limits on career choice, the societal impacts can be felt in many aspects of Canadian life:

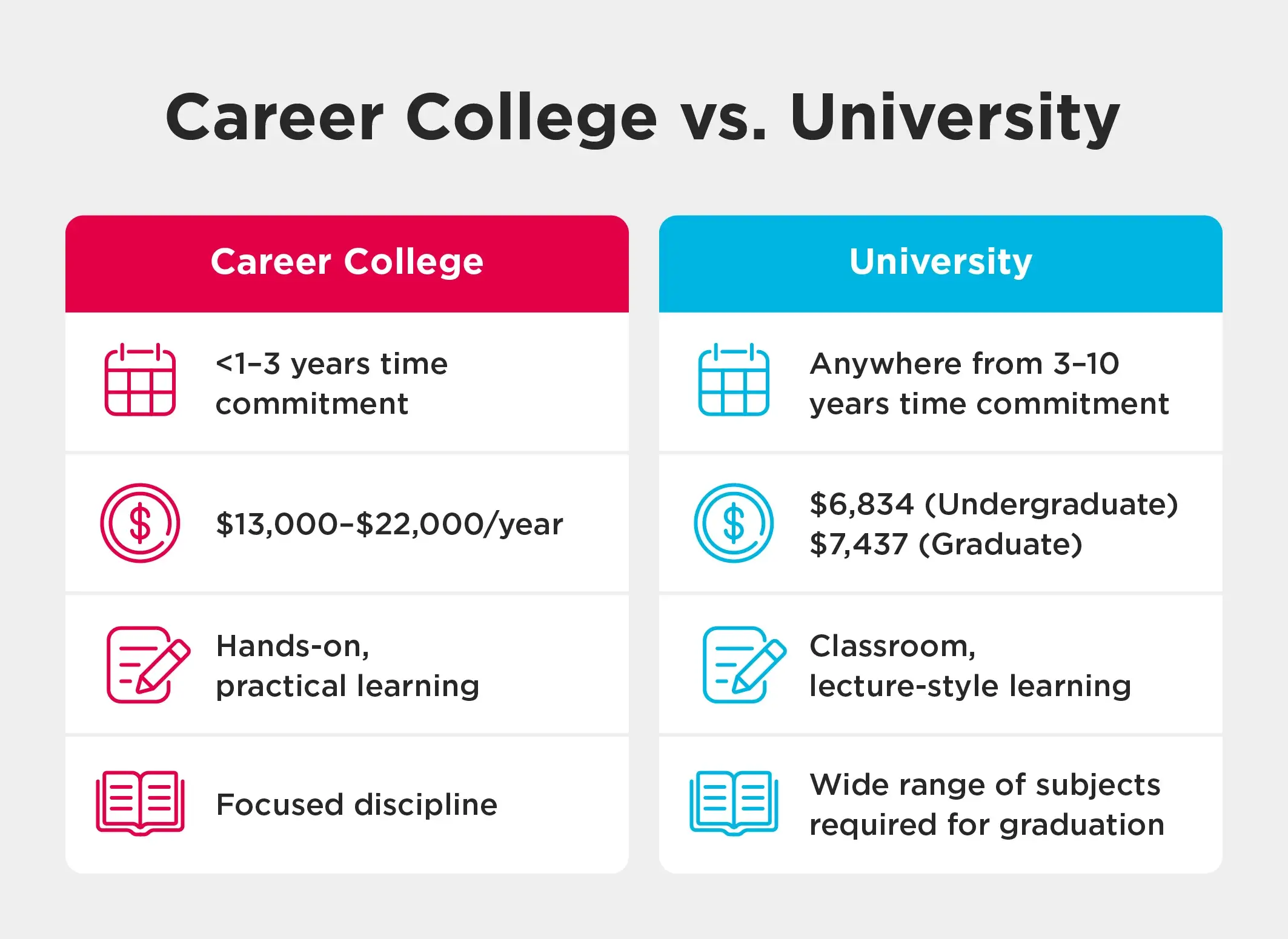

Many students increasingly favour career colleges versus universities, where they can start working in their field in as little as one year (or even less) and take on less debt, even if they require student loans.

Career colleges often take less time and, therefore, cost less in the long run. There are benefits to each, but the main benefit of a career college is its focused educational approach that teaches students the skills they need to get a job in their field. Universities take a broader approach to education, where students are required to take a wide range of courses, not just their chosen focus.

With focused programs and real-world course offerings at career colleges, finding employment after graduation may also be easier, which can help avoid debt accumulation.

The average student loan debt in Canada is $28,000. This takes into account all program and discipline types in different provinces, including both universities and colleges.

It depends on the level of university education. For undergraduate and Master’s students, the average debt is $28,000. For a doctorate, the average debt is $33,000.

It takes an average of 9 1/2 years for Canadians to pay off their student loans.

The average third-year Law student has $71,444 of student loan debt in Canada, according to Canadian Lawyer magazine.

Ontario has the highest amount of student loans, followed by Alberta and British Columbia. Yukon has the lowest amount of student debt. These figures are relatively in line with the population.

The Government of Canada eliminated interest on all federal student loans. However, some provinces still require interest payments. Most use Canada’s prime rate as their basis, which is currently 7.2%.

According to Statistics Canada, Dentistry has the highest tuition fees, followed by Medicine and then Veterinary Medicine.

A normal amount of student loan debt is anywhere from $10,000 to $30,000, depending on the area of study and level of education.

With the average student loan debt in Canada on the rise, it’s no wonder so many are turning to career colleges like Robertson to learn the practical skills that will get them working faster in their desired career

Are you looking to get started on your career journey? Speak with a Robertson advisor today.

In This Article

The first few years of life are full of many milestones and can set the tone for how a person learns and interacts with others for the rest of their life. Early childhood education helps children learn how to build relationships and resolve conflict. Not...

What’s the first thing that comes to mind when you think of an Accountant? Probably math. Maybe someone you know who is an Accountant. But the word interesting may not be the first thing you think of. You would be wrong. There are many accounting...

We often talk about courses to explore, potential careers, and the key to success in a job. However, we sometimes overlook the educators who guide us and the programs that help them get there. The best education programs in Canada are ones that keep their...

Once you take the first step, one of our Student Admissions Advisors will get in touch to better understand your goals for the future.

Apply Now